Last week I looked into the ways that the Supreme Court’s June ruling that declared Section 3 of the Defense of Marriage Act unconstitutional impacted marketers. While the decision sent ripples of relief through the pro-same-sex marriage camp, these ripples became waves of confusion when seen through the eyes of health insurers and employers trying to make sense of the new rules.

Last week I looked into the ways that the Supreme Court’s June ruling that declared Section 3 of the Defense of Marriage Act unconstitutional impacted marketers. While the decision sent ripples of relief through the pro-same-sex marriage camp, these ripples became waves of confusion when seen through the eyes of health insurers and employers trying to make sense of the new rules.

{kind=link}

DOMA Decision Defined

Section 3 of DOMA prevented the recognition of same-sex married couples under federal law, and effectively banned them from receiving federal benefits extended to married people. With the Court’s decision that this part of DOMA is unconstitutional, the door opened to same-sex married couples to receive federal benefits — but it’s what the Court didn’t address that’s causing confusion.

Section 2 of DOMA, which the Court did not negate or even mention in its ruling, allows states to refuse to recognize same-sex marriages that are performed in other states. The ruling also didn’t address state laws that prohibit same-sex marriage. This makes for murky waters in cases where there’s a question of which state’s law applies to different situations when deciding whether a same-sex marriage qualifies for federal benefits.

Questions and Issues

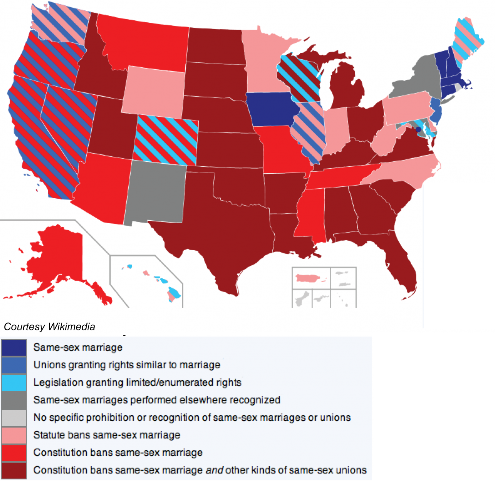

Currently, 14 states and the District of Columbia allow, or will allow later this year, same-sex marriage; 6 states have laws prohibiting same-sex marriage, while 29 states have constitutional bans in place. Adding to the confusion is the fact that each state has different rules for determining which state’s law to apply to different cases.

For example, a same-sex couple legally married in one state, but living in a state that doesn’t recognize same sex marriage, may cause confusion for a health plan administrator who doesn’t know which state’s rules apply. If a same-sex married couple moves from a state in which they’re eligible for benefits to a state that doesn’t recognize their union, they may face tax and health benefit changes.

For example, a same-sex couple legally married in one state, but living in a state that doesn’t recognize same sex marriage, may cause confusion for a health plan administrator who doesn’t know which state’s rules apply. If a same-sex married couple moves from a state in which they’re eligible for benefits to a state that doesn’t recognize their union, they may face tax and health benefit changes.

Another area in which there’s a lot of confusion is whether or not the DOMA decision will be retroactively applied to benefit decisions made before the Court heard the case.

In states that recognize same-sex marriage, the following benefit changes will apply:

Group Health Plans

Employer-provided health care coverage for spouses and their children is generally a pre-tax deduction, reducing the amount of income on which the employee must pay federal tax. However, DOMA prohibited employers from applying that practice to same-sex marriage, meaning that employer-provided coverage counted as additional, taxable compensation.

The Supreme Court decision removes this rule, allowing same-sex spouses and their dependent children to be counted as spouses and stepchildren the same way heterosexual marriages are considered. This may provide a tax break for many employees, and they may even be able to file claims for refunds on federal income tax paid on spouse and dependent health benefits.

Additionally, employers and employees may both be eligible for refunds on FICA taxes paid on these benefits in previous open years.

Flex Accounts

Just like with group health plans, pre-tax flex account coverage was unavailable to same-sex spouses and their children, unless they were otherwise qualified as dependents under federal tax law. With Section 3 of DOMA struck down, employees can receive pre-tax flex coverage for their same-sex spouses and dependents.

COBRA

Same-sex spouses will now be able to claim beneficiary status for health care continuation coverage, including after a divorce.

Special Enrollment Rules

In some cases, employers may be required to give same-sex spouses and their dependent children immediate special enrollment to employer-provided group health care plans. They might also have to provide change-in-status eligibility under cafeteria health plans.

While questions remain as to how rules are going to be applied between states, employers in states that recognize same-sex marriage need to start the transition process. Hopefully, the Labor Department and IRS won’t take too long to provide extra guidance on the new rules, and how to apply them.

Elizabeth Gooding is the editor of the Insight Forums blog and president of Gooding Communications Group www.GoodComm.net